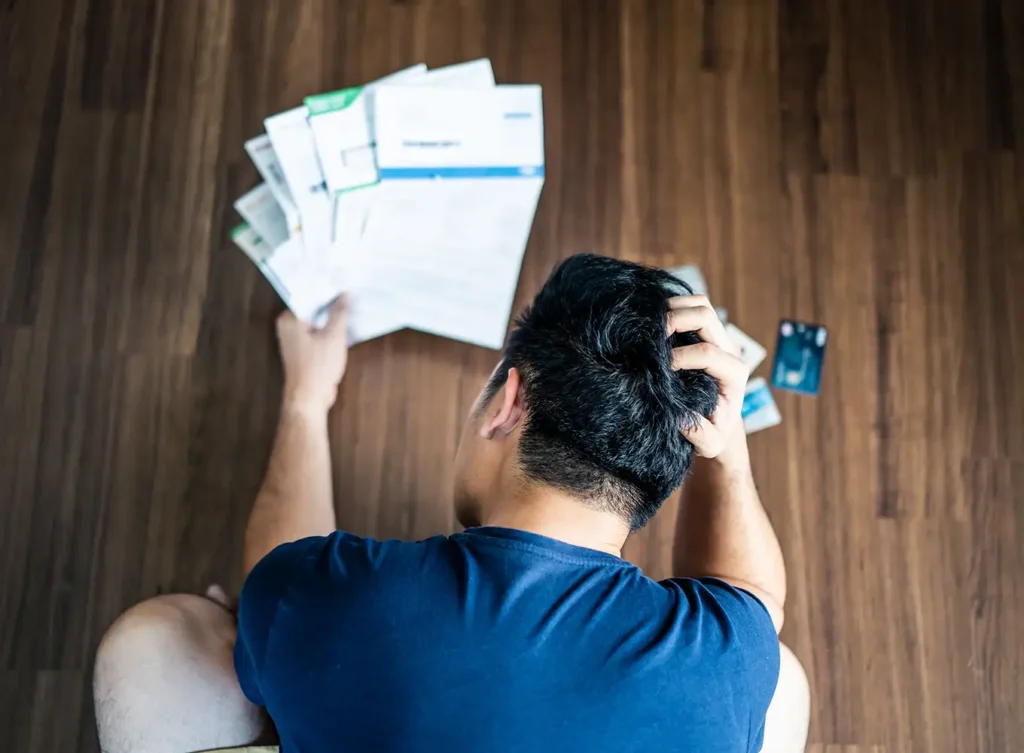

Debt Consolidation Loans

Many finance companies and banks offer loans to consolidate all or most of your bills into one “easy” payment. These loans are often made by a lender or finance company you already have accounts with. Sometimes the only reason the loan manager is being so generous is to get a sales commission on your account.

Consolidation Loan Pitfalls

Lien Risks & High Interest Rates

Only rarely are these loans a “good deal.” Many of these lenders take a lien against your cars or household goods. The idea is to hold these personal necessities “hostage” to guarantee your repayment. Often, the interest rate you pay is actually higher than you were paying before on the separate accounts — sometimes in excess of 20%. The monthly payment is only lower because you have promised to pay for a much longer time — which means you are paying a lot more in the long run.

Long-Term Costs

Calculating the True Expense

A little simple math should tell you why these are bad deals. A $10,000 consolidation loan for 10 years at 18% may have payments less than $200 but it means you are paying more than $20,000 over the loan’s life. $5,000 over 5 years may be less than $150 per month but ends up costing you more than $7,000 in principal and interest payments. Worse, many of these lenders try to sell you insurance which will make the payments to “protect” you in case of emergencies. Credit life and credit disability insurance is very expensive, very hard to make claims on, and mostly protects the finance company. These policies can add several hundred dollars to the amount you finance — and how much you end up paying.

In contrast, many of the debts you could consolidate this way — credit cards, medical bills, finance company loans — could be wiped out completely or paid back pennies on the dollar in bankruptcy without putting your cars or household necessities at risk.